Spotlight on Rare Diseases: How Well Do You Really Know Your Health Care System? A United States Perspective

Read the introduction to this series for context.

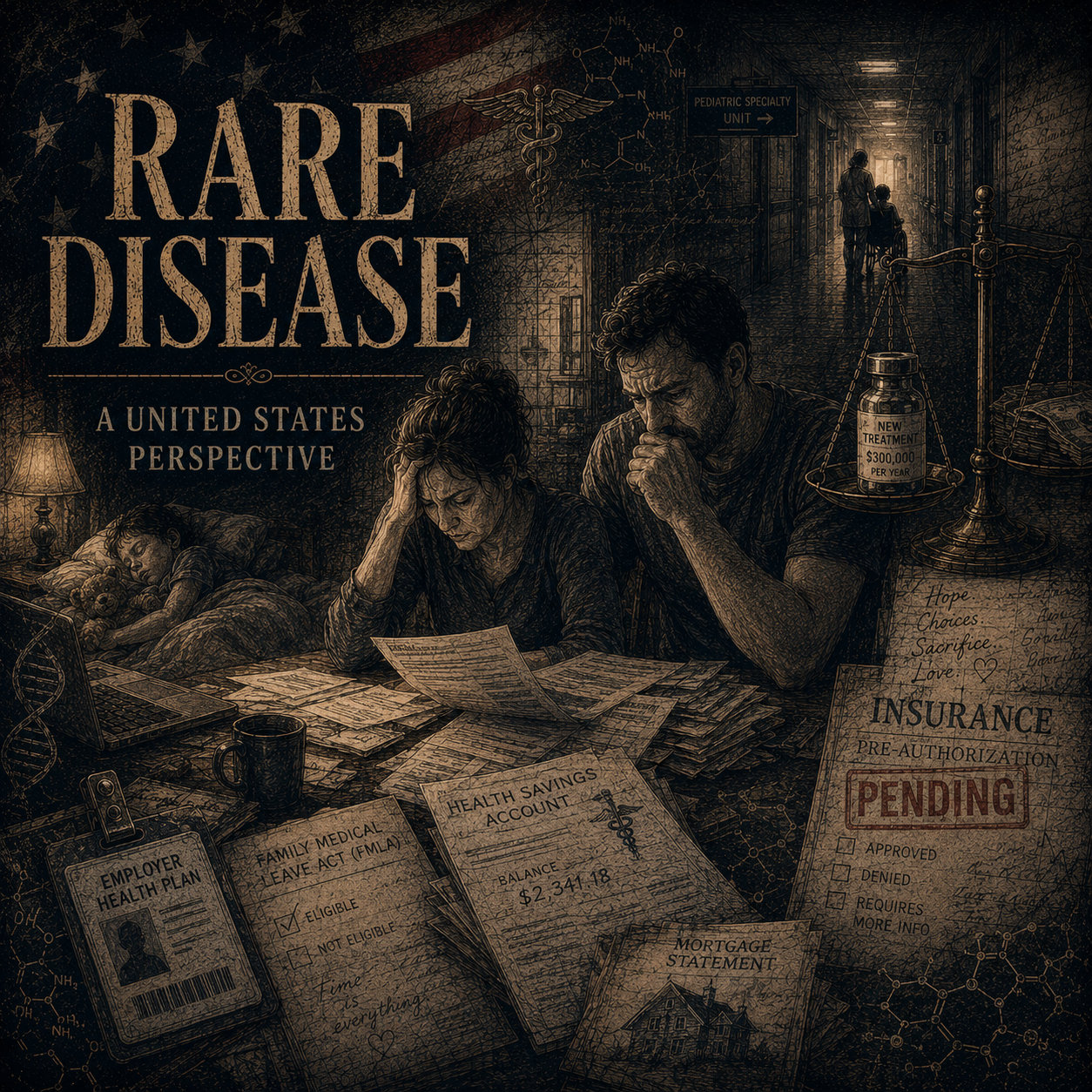

Your child is sick and should receive treatment as soon as possible because you want them to have a chance at a long, healthy, prosperous life. You are willing to do whatever it takes to make that happen. But in the United States, health care is rarely straightforward. “Whatever it takes” will be cumbersome, time-consuming, anxiety-inducing, and may still not be enough.

“Health care in the United States is complicated and access to care depends on so many factors it is daunting for a family unfamiliar with the system to navigate it,” said Rachel Povhe, Health Insurance Navigator with the Healthy Community Alliance, a rural health network in western New York. “Insurance navigators are able to help with this process because we know the system well, but success in securing coverage is dependent on many factors including income and household size and could be unaffordable.”

Health insurance in the United States is complex and typically categorized as either public or private. Public health insurance includes Medicare, health coverage for those 65 years-of-age and older; and Medicaid, insurance for those with limited resources. Private insurance includes employer-sponsored health insurance plans or direct purchase plans.

No matter which coverage option you have, you likely have to pay some percentage of the cost for that coverage. Most coverage is incomplete. The U.S. Consumer Financial Protection Bureau (CFPB) and the Kaiser Family Foundation (KFF), a health policy organization in the U.S., note that “most health plans only provide 80% payment for covered costs. Approximately 14 million people (6% of adults) in the U.S. owe over $1,000 in medical debt and about 3 million people (1% of adults) owe medical debt of more than $10,000.”

In your situation, with a salaried job paying a bit more than the US median, your insurance coverage is likely comprehensive enough to cover the costs of treatment for your child. You wonder, though, if it will cover all the costs, like the physiotherapy and home care, associated with their treatment and for how long?

You also must consider how this will affect your career. You’re looking toward career advancement that might require changing companies, but you have to wonder whether you can make this change, because it will likely lead to a change in insurance companies and maybe a change in what’s covered and what percentage of the cost you must bear yourself. That’s a chance you may not be able to take. Employers often have a waiting period before health insurance takes effect for new employees, sometimes as long as 90 days. With a sick child, you cannot be without insurance for even one day.

You will also have to make sure you are eligible for the federally mandated Family Medical Leave Act (FMLA) program, if you want to have the flexibility to care for your child. Qualifying for this program means you must work for a company with at least 50 employees (or for a public agency like a school or the government) and have worked with that employer for at least 1,250 hours (about 35 weeks).

While the Affordable Care Act (ACA) nearly eliminated the need to worry about pre-existing conditions, that is not a guarantee. You would not have to worry about this with the health plan at your current employer. With your youngest child’s condition, you and your family are going to have to make changes. You begin to worry that your older child may have to give up their beloved extracurricular activities because you may not have the resources for them to continue. You talk with your partner about pausing your small business dream to care for your younger child. You continue to weigh all the options given that you will likely have additional unforeseen costs, in terms of both time and money.

Most healthcare practices have departments dedicated to handling insurance related matters, such as pre-authorization for procedures and submitting claims. But, even with this level of expertise, pre-authorization is not guaranteed. It is likely that you are going to have to figure out how to manage the health care system to some degree on your own. Certainly, you will need to become your child’s advocate.

You and your family are lucky because you are near a facility that can provide the treatment your youngest needs and has a specialist adept at maneuvering the insurance landscape. That is not always the case. Health care services vary widely across the country.

Your child may also qualify for additional services through other agencies, such as a department of social services or an office for persons with disabilities. This multi-agency approach can potentially lower some costs and provide information about how to access resources like physical and occupational therapy, as well as any medical devices required. These offices may also be able to help you manage the insurance landscape and potentially get these services covered through your insurance or Medicaid. This process, however, typically takes a significant amount of time. Time your child doesn’t have.

It appears you have some good news. Your child’s physician told you that insurance will cover the cost of the treatment. They will also cover the cost of any necessary assistive devices and physical and occupational therapy. They will not, however, cover the cost of any in-home care your child may need.

This means that your elder child will be able to continue with their extracurricular activities, as you and your partner have made that a priority. You and your partner agree to start the therapy and agree to use your health savings account (an account you contribute to at work to help pay for qualified medical expenses) to fund it. You do have to talk about home care options though. You reach out to your county office of social services for assistance. They believe they can help you secure that care for a couple of days a week, but the approval process will take several months. Your partner’s small business, in the meantime, has gone on the backburner. Money will be tight until the home care support comes through if it does.

You can breathe a bit easier, because there is more help available than you’d feared, but you do worry about the future. Will your insurance continue to cover this expense? Are you now trapped with your current employer forever, with your wages potentially stagnating? Will a new treatment ever be available that will be less expensive and more effective? You are glad you’ve figured out a way to get your child the care they need and keep your head above water for now. But life is never going to be the same. Your child’s health will forever be precarious, as will your financial security.